Before taking out a loan, learn the differences between these two types, which has better interest rates, and which to get in certain situations.

If you want to borrow money, you have several options in Canada, including a secured or unsecured loan. These loan types have several things in common. Off the top: Financial institutions will lend money for a certain period of time (a.k.a. a term), both types require a credit check and both charge interest.

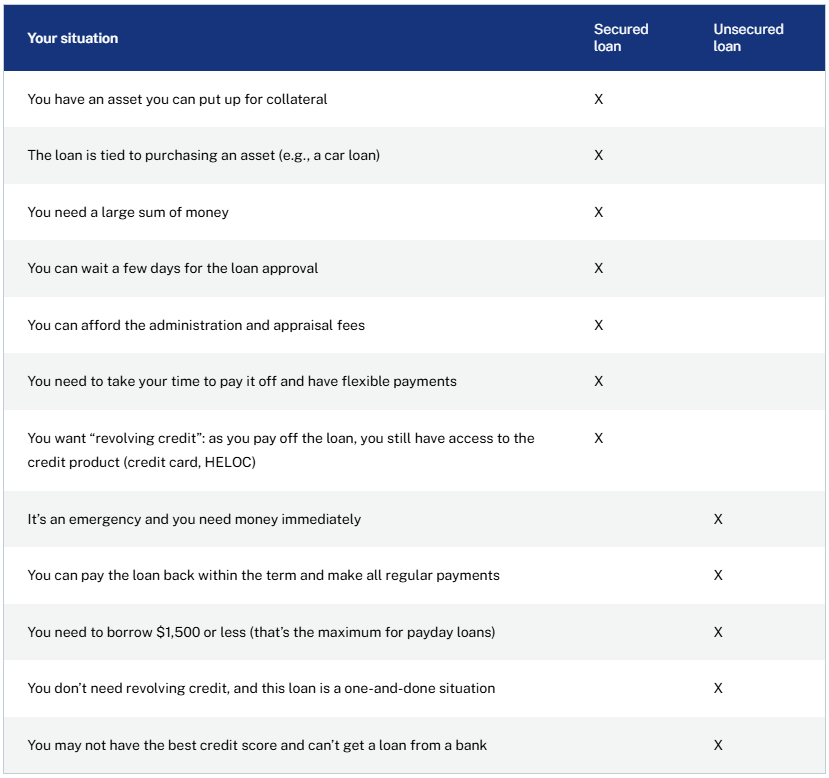

When comparing secured loans versus unsecured personal loans, look at each loan’s pros, cons, risks and benefits. You’ll also want to look at how your financial needs, your situation and your personal goals can come into play. Understanding the differences between these two loan types is key, because you can make the best financial decision before you borrow money.

What is a secured loan?

A secured loan is one that is backed by collateral using your assets. You can use your home, car or another piece of property you already own as a lien against the money you’re borrowing. If you default on the loan (meaning you don’t repay it), the lender, usually a financial institution, can take the asset you’ve put up as collateral.

This collateral reduces the risk of the bank or other lender losing that money, which ultimately means you can borrow a larger amount of money for a longer term, often at a lower interest rate, than you could with an unsecured loan. That’s because the lender isn’t taking a huge risk on you when they lend the money.

Getting a secured loan is good for bigger items like home renovations, a vacation (but we recommend saving for that), a wedding, and debt consolidation for high-interest debt like credit cards. A secured loan can also be used for post-secondary education if you don’t qualify for an education loan. An auto loan is one example of a secured loan—the car is the collateral.

What is an unsecured loan?

On the other hand, an unsecured loan doesn’t need collateral. There’s more risk to the lender because there is nothing to guarantee it will get its money back, so borrowing amounts tend to be lower and the interest rates tend to be higher. These loans are best reserved for expenses like emergency home repairs. A payday loan is an unsecured loan as there is no collateral and a high interest rate.

When done smartly, an unsecured personal loan can actually help you save money. If you hold a credit card (unsecured loan) with a high interest rate (22.99%!), a personal loan can help you pay off that debt faster. You’ll have to repay the personal loan, of course, but the lower interest rate means you’re paying less money for credit over time.

The pros and cons of secured loans

Like all loans, secured loans have advantages and disadvantages.

Pros

The advantages of a secured loan are:

You have a higher chance of getting approved since you’re putting up collateral, which minimizes the risk to the lender.

The interest rate may be lower, making it more affordable for you to pay off the loan over the period of the loan term compared to an unsecured loan.

You may get a larger amount of money due to putting up collateral.

Cons

The cons of getting a secured loan are:

You could lose your asset if you default on your loan.

You might have to pay additional fees like an administration and appraisal fee for your asset, so you pay more or you get a lower loan amount if the fees are deducted from the approved amount.

It takes a few days to be approved because the lender needs to verify and approve the appraisal.

If you default on the loan, your credit score and credit reports will take a hit.

The pros and cons of unsecured loans

Before you sign up for an unsecured loan, check out the benefits and risks.

Pros

You don’t need collateral, so if you default on the unsecured loan, you won’t lose an asset.

The application and approval are usually fast, often taking minutes or at most a day with many lenders.

Your loan is a sum of money not tied to a home or vehicle (unlike a mortgage or car loan), so you can use that cash for anything.

Cons

It can be harder to qualify for an unsecured loan than a secured loan. The risk is higher to the lender.

That also means the interest rate may be higher compared to a secured loan.

Your credit score may need to be good, very good or excellent, ranging from 650 to 850.

The borrowing amount is smaller compared to a secured loan.

If you default on the loan, your credit report and credit score will be negatively affected.

Before you decide on a secured vs. unsecured loan

There are several things to know before taking out a loan, whether it’s secured or not.

Read the contract thoroughly before you sign anything. Make sure you know the terms of the loan, the interest rate as the annual percentage rate (APR), and whether the rate is fixed or variable. If it’s fixed, you know how much you have to pay each pay period, as it’s the same amount. If it’s variable, your payments will change depending on the Bank of Canada’s overnight interest rate (more on this in the next section). So if the overnight rate goes up, you may pay more each pay period or a greater portion of your payment goes towards interest versus the principal.

Speaking of payments, check if you can afford them. Consider how much you want to borrow, how much you can afford to pay back each month, and whether you can still afford the payments if the interest rate rises.

For secured loans, make sure you are comfortable with the terms. You don’t want to default and lose your collateral asset. That means losing your house, car or other property. Your credit report and score will also be affected, making it harder to get another loan.

How interest rates work for secured and unsecured loans

Interest rates are the cost you pay to borrow money. When you take out a loan from a financial institution, you can expect to pay back more than the amount you were given.

These rates start from the Bank of Canada’s overnight lending rate, also known as the policy interest rate. That rate informs the prime rate for Canadian banks. (The policy interest rate is currently 3.25%.) So, when the overnight rate goes up or down, the prime rate changes in response. This affects interest rates for products like credit cards, lines of credit, auto loans, and other secured and unsecured loans. Financial institutions will offer fixed or variable rates for various loans.

Other factors that affect interest rates for secured and unsecured loans come from the borrower. If you’re applying for a secured loan, you’re offering up an asset for collateral, so your interest rate may be lower than it would be for an unsecured loan.

Also, the higher your credit score is, the better your chances of getting a more favourable interest rate.

Lenders also consider your debt-to-credit ratio. That’s the amount of credit you’re using divided by the amount of credit you have. If your ratio is below 30%, you may have a much better chance of getting a low interest rate.

Other types of loans

Under secured and unsecured loans sit other types of loans. Here are a few examples.

What are HELOCs?

A home equity line of credit (HELOC) is a type of secured loan. Your home is the collateral. Most HELOC loans only require you to pay the monthly interest on what you borrowed—meaning your payment schedule may be flexible (aside from the interest of course). That minimum amount covers the interest. You can take as long as you need to pay off the HELOC, but know that the longer you take, the more you will pay in interest. Current HELOC rates are sitting at 6.45%.

What is a payday loan?

A payday loan is a short-term unsecured loan with a high interest rate and high fees to borrow. There’s no collateral, but if you don’t pay the loan back quickly, you will rack up a lot of interest in a very short time. Payday loans in Canada can have a maximum yearly interest rate of 442%.

Which type of loan should you get?

Getting a loan in Canada

If you’re thinking of getting a personal loan, make sure you understand the loan agreement, borrow only what you need and do your best to pay it back within the term. If you need help with your overall financial well-being, consider talking to a financial advisor. This all helps you achieve your financial and life goals and can even boost your credit score, making it easier the next time you need another loan or a mortgage.

SOURCE AND FOR MORE INFORMATION: CLICK HERE